Avocado on toast, as it turns out, is not what’s causing Australians to feel more worried about their financial future than ever before.

We have a growing cohort of the population heading into retirement over the next five years who have to wait longer to be paid a pension, and fears within the younger workforce that they will be working longer than their predecessors while being increasingly put in charge of managing their own retirement funds. Financial shifts like these are a result of years of economic movements, and there is little point in blaming the moon for the tide.

However, only 27% of Australians have ever received financial advice. This is not because we’re educated on financial concepts throughout our lives or that we’re given the toolkit to manage finances. In fact, data shows that we score lower on financial literacy than comparable countries and that many more see the value in financial advice. But there are Australian-specific barriers to engaging with financial consultancy that can counter the disadvantages many younger Australians face.

Australia’s low financial literacy rates (the understanding of financial concepts and how they play out in the real world) are one barrier to better retirement planning and aged care. Women and lower socio-economic classes are at a steeper disadvantage with gender and class gaps further reducing their financial literacy rates and affecting their ability to counter the disadvantages. Alongside this, Australia’s stigma around personal finances inhibits the free flow of knowledge that can help us optimise our money, early and intentionally.

Over the years, policymakers have leveraged Australia’s self-sufficient attitude to many aspects of life and livelihood to drive self-efficacy in retirement planning, yet they have not filled in the knowledge gaps for the workforce. This culture of self-efficacy leaves Aussies with a lack of awareness of assistance programs, not knowing where to go for help and not knowing who to trust. It needs to change in order for us to become a nation that can deliver the income needed for a comfortable retirement after a career of hard work.

Isolated in confusion

From a cultural standpoint, Australia is conservative about personal money matters, and there is a negative class stigma that inhibits Aussie consumers and households from asking for help. We’re encouraged to achieve the nuclear family with picket-fence housing, and homeownership is a life goal for over half of Australians, no matter how long it takes to pay it off.

With such high financial goals, it would make sense for it to be a hot topic of discussion. But 28% of Australians don’t like talking about their finances openly with others, the topic comes only second most uncomfortable after sex. 96% of Australians have experienced financial hardship, and as the topic comes with shame for many, Australians are isolated in managing their finances, paying off their mortgage and planning for their retirement.

Breaking down financial literacy

Before we get any further into breaking down the impact of illiteracy rates on Australian retirement funds, let’s directly break down the stigma.

In a study of Financial Literacy and Retirement Planning in Australia, Agnew et al. implemented a survey to measure financial literacy in a range of countries and relate it to retirement planning. Their benchmark for financial literacy is measured against consumer understanding of three tenets: inflation, interest and risk diversification. Below, we’ll briefly explore these tenets and how they impact money management.

Inflation

Inflation is the rate of increase in goods and services over time. It won’t tell you the exact increase rate of eggs over the last year, it should be looked at as more of a broad measure of the rise in the cost of living in a country. It’s considered to be positive for the economy and is caused by a matrix of factors. Without knowing inflation rates, the workforce is financially worse off in many ways, one example is that workers aren’t motivated to negotiate higher wages and salaries to combat inflation.

Interest

Interest is the money it costs to borrow money or the money earned in lending money. Banks pay interest when you hold money in an account with them because they technically have access to this money to lend to others. This can sound like a good deal, but your interest rates are competing with inflation where $10 yesterday means more than $10 today. This is why many financial advisors would encourage you to invest instead of save because investing in the economy itself means your money grows with inflation. Of course, it’s not that simple when you’re investing in the growth of one company, which introduces the concept of risk diversification.

Risk diversification

Risk diversification refers to the splitting of your investment portfolio across different companies and industries. By diversifying your investments, you mitigate the impact of when a company or industry you’ve invested in regresses because the remainder of your portfolio should increase enough to more than cover the losses.

Learning these concepts is foundational to Australian consumers being able to make their money work for them and for the economy.

Australians are among the least knowledgeable in financial literacy and retirement planning

By default, we exist within our economic system. There isn’t a step to take that leverages us into the merry-go-round, we’re either actively involved or passively. It should follow then, that financial literacy and education should be an inherent part of education, so we can all take active steps to optimise our income early and live comfortably in retirement. While that makes logical sense, it’s not the reality.

So where does Australia place in Agnew et al.’s study against the three tenets of financial literacy?

Their data shows that the average Australian’s financial literacy is the equivalent of “the young, least educated, unemployed and those not in the labour force most at risk, of comparable countries”. While their knowledge of inflation and interest is on par with that of other surveyed countries, they fall behind in risk diversification knowledge.

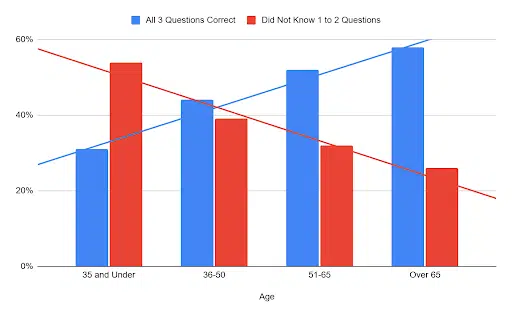

What Australia’s age literacy rates tell us

Australians start behind comparable countries, but the trend line in the graph above shows that our knowledge increases with age. The over 65 category scores close to other countries, with over half of this cohort answering correctly in all three categories. As Australians approach retirement age, their growth in financial education may stem from the pressure of saving for retirement, just as their years earning an employment income that could have had a powerful impact on their retirement come to an end.

For younger Australians, more than half of those aged under 35 showed a lack of understanding in one or two of the three categories. Young Australians without a proper understanding of financial concepts are working within an economy that has seen inflation rates over the past three years at three times the average and a wage price index far below. With this financial illiteracy, there is little opportunity to counter the economic conditions other than use their savings to pay their bills, leaving increasingly less left over to invest in their future at a time in their lives when it will produce the biggest retirement dividends.

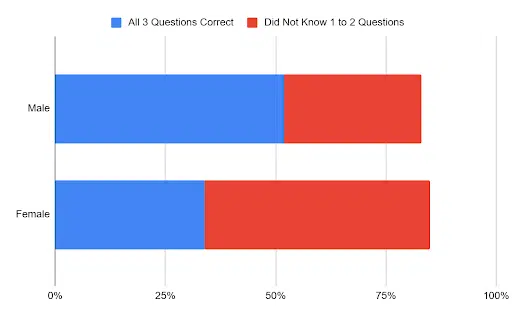

Women have lower literacy rates which impacts their retirement funds

There is also a dramatic difference in financial literacy in the gender category. Around 34% of women demonstrated an overall understanding of interest rates, inflation and risk diversification as the three tenets of financial literacy. During retirement, the ABS tells us that this gender gap continues, with superannuation contributing to 33% of income for men and 21% for women.

Yet, Australians are increasingly pushed to take responsibility for their finances and retirement

Australia’s culture has long been known for its pull-yourself-up-from-your-bootstraps mentality and valuing self-sufficiency. This lack of interpersonal dependence and community values plays into the culture of you-can’t-talk-about-money, and it has also paved the way for policies moving away from retirement plans and pensions and Australians being increasingly pushed to manage their own retirement.

In The Australian Journal of Management’s study, the authors state that “ there has been a push to make [you] responsible for [your] own financial retirement planning in an environment of greatly increased longevity, a declining number of employer pension plans and defined benefit pensions (Holzmann, 2013) and an increasingly complex financial services industry.”

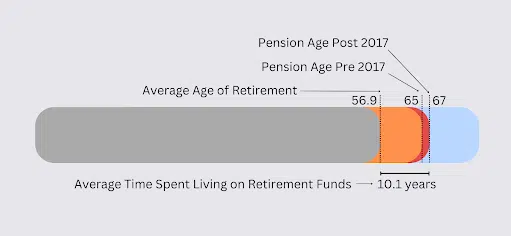

The average age of retirement for Australians is 56.9 years old. In 2017, the minimum age to qualify for a pension increased to 67 years old. This means that there are 10 years that retirees need to live off their superannuation on average, which is the longevity the researchers are talking about. If you’re currently in employment, it’s hard to visualise and estimate how much money you will need to retire and live comfortably in ten years, but anywhere between a couple of hundred thousand to just under a million dollars constitutes a comfortable retirement. It’s no wonder only around 30% of retirees have enough for the retirement they had planned for.

Experts are also estimating a retirement surge in the near future, with a spike in the number of people set to retire in the next five years. For younger people, the sentiment seems to be that the pension age will increase further “unless the government can meet the financial requirements of the growing cohort of retirees.”

These factors increase the need for workers to seek professional financial advice. Yet financial illiteracy itself is a barrier to engaging with financial advice. Many people want to hold on to as much savings as they can, which, for many, is misguided financial management, as they could be seeking advice, investing or contributing to their superannuation.

How illiteracy affects retirement planning in Australia today

Aussies are putting off our retirement plans

75% of Australians find the retirement system complex, fueling a lack of confidence in having enough income during their retirement to live comfortably. Retirement literacy is directly related to financial literacy, and with this literacy, Aussies could turn to better retirement planning measures. Instead, they are planning to retire later in life than ever before, as the workforce believes they have to earn more lifetime income instead of optimising their money and are anxious that the retirement age will increase again before they reach that age.

We had an open-source experiment on the attitude towards retirement funds recently when the government enabled early access to superannuation during COVID-19. While this was necessary for some to pay bills, financial illiteracy may have caused others to access it without knowing the risk to their retirement fund as 12.5% of people who made deposits put it in their savings account.

Even more recently, the approved First Home Super Saver Scheme has allowed aspiring home buyers to withdraw from their voluntary contributions in their superannuation to help pay for their home. However, anyone is free to make voluntary contributions to their superannuation, so all that this scheme does is incentivise Australians to contribute to their superannuation so that the money is invested into the Australian economy. While early contributions to superannuation are a powerful way to grow retirement funds, as the scheme only allows you to withdraw it for a mortgage, it leaves younger Australians locked into a, sometimes life-long, debt.

Over 5 million Australians have struggled to make their loan and debt repayments. When we consider this volume of people and the sheer size of mortgage debt, we can see how loans are irresponsibly pushed beyond people’s capabilities. And with enforced self-efficacy and stigma around money matters, Aussies aren’t asking for help. This scheme leverages the self-efficacy in personal finances that Aussies are bound by while harnessing financial illiteracy to take from their retirement funds and invest in a multiple-decade debt that will rule their working life.

Financial illiteracy in men vs. women

The gender financial literacy gap affects many women in retirement. However, the gender gap in other areas contributes to a less prosperous retirement for women on average, too. Many cultural and policy factors contribute to women earning a lower lifetime income, and as proportional salary contributions are currently the only compulsory funnel into superannuation, it leads to a lower income for women in retirement.

Some examples of how the gender gaps cause a lower lifetime income for women include:

- 65% of women who worked as employees while pregnant took unpaid leave

- Reduced future earning capacity with children

- Minimum wage maternity leave

- Divorces that leave women at a disadvantage after gender financial and social gaps reduce their superannuation

With an even lower rate of understanding concepts like compounding interest and risk diversification in investments than men, there is little motivation to prioritise superannuation, even if their income allows them to make contributions, which is a markedly lower possibility for women. On top of this, the average woman in Australia is less likely to seek out advice due to gender bias. This is why women financial planners and advisors are critical.

Barriers to financial literacy and advice

We don’t know what we don’t know. Socrates’ phrase echoes through the financial realm, where the wealthy benefit from the lack of understanding of the remainder of the population. Without knowing where your money is best placed and why, you default to giving it to someone else to grow it for themselves like your bank using your deposits for their own lending power. Thus, financial illiteracy itself is a primary barrier to expanding your financial literacy.

Beyond this, many Australians distrust financial institutions. They know these institutions are making money from them, so they’d prefer to keep their distance. This mistrust is amplified through media-lead fear-mongering where scandals, as you would see across any industry, are emphasised, knowing personal finances are a sore and triggering point for viewers and readers. This has compounded the ‘Us vs. Them’ situation between the finance sector and the rest of Australia. When all of this is mixed in with a lack of financial education in the schooling system, Australians are in a bind where they remain uninformed and have a distrust holding them back from acquiring the knowledge that will help them live a prosperous retirement.

Boost your financial literacy to prepare for Australia’s cultural shift on all things money management and retirement planning

As Australians, we need to create a shift in culture. If we are thrust into self-efficacy to build a retirement fund, then continuing the narrative that supports money stigma and financial illiteracy is doing us all a disservice. Instead, we can work together to share knowledge and educate ourselves, removing the remnants of media-lead distrust and seeking advice for the benefit of yourself and your well-being in retirement.

On an individual level, illiteracy like not understanding risk diversification indicates that Aussie consumers may struggle with the concept of superannuation and the safety it offers in investment diversification. Realising that financial illiteracy may be holding you back from seeking advice and education and keeping you in a financial cycle that you can’t leverage your way out of can be enough to dismantle the barrier. From here, you can start to bolster your financial literacy by seeking advice that will benefit your retirement and optimise your money as early as possible so you have the means to manage your retirement responsibility proficiently.

Ultimately, Australians do want to engage with and see value in financial advice, but distrust is the main barrier. The best step you can take is to begin educating yourself and finding the right support. Get started with your own learning today with our Hints & Tips or you can explore our suggested books or podcasts to financially upskill and optimise your money for retirement.

For anything else, contact our team at Best Financial Planners and we’ll be in touch with more information.