Assets

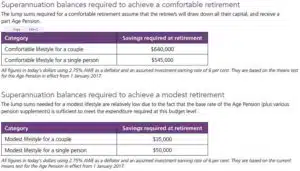

The AFSA (Association of Superannuation Funds of Australia) has made a calculation of the necessary superannuation balances for retirees aged around 65 to help them attain their incomes. When it comes to assets, it is assumed that all capital is drawn down by the end of the retirement period. This is exclusive of personal assets and the family home, which doesn't leave much superannuation for beneficiaries.

The calculations factoring in Centrelink Age Pension assumes that, for instance, a couple wanting a comfortable income upon retirement would need a superannuation of $545,000 at least for every person. The estimation is, however, oblivious of your personal and financial circumstances, so consult a qualified financial planner if you have uncertainties about your retirement planning.

Source: Super Members Council of Australia, formally AIST

If you are planning to have a comfortable retirement income, it's advisable to consult a qualified financial planner to guide you. The information and research on this page is just a guide, and it doesn't consider your personal preferences and financial situation, so it might not be specific to you. There are financial planners in different cities and states, and you can find them using the website menu located at the top of the page.